Brazil is not for beginners (see previous post). It may be the first time in history in which anti-cyclical policies actually caused a recession, instead of pulling the economy out of it. Another hit for the paradoxical middle-income country in which aggregate taxes are on par with developed countries, tax collecting is more efficient than almost anywhere in the world, and government expenditure is wasteful and incompetent. In 2013 I wrote an article praising the Brazilian balanced budget, which was enshrined into law (Lei de Responsabilidade Fiscal – LRF) in 2000. In its essence, the Brazilian Balanced Budget Act is a simple one: it ensures that the country cannot run a primary deficit. It is not cyclically-adjusted, and has worked as a hard cap till 2014, when the Brazilian government run a primary deficit for the first time since the inception of LRF.

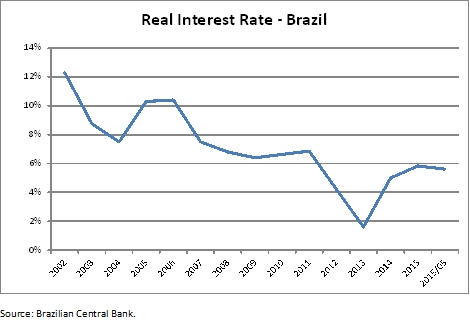

The Balanced Budget Act is a major structural reform that helped bring down real interest rates in Brazil, which dropped from 12% a year in 2002 to less than 6% in 2015. This rate is still much higher than in most emerging countries, the legacy of mistakes past. Yet, given Brazil’s history of fiscal woes the downward trajectory of real interest rates looked promising, with a brief period in which real interest rates flirted with the 2%p.a. barrier.

In 2012-13, Brazil had a major window of opportunity to consolidate its fiscal standing and establish a period of permanent low real interest rates. The government blew it by putting in motion one of the most inefficient programs of public spending in the history of the country. The result: a recession caused by expansionary fiscal policy, of all things.

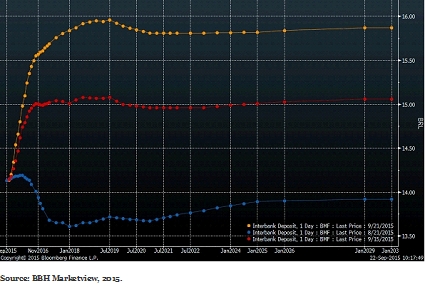

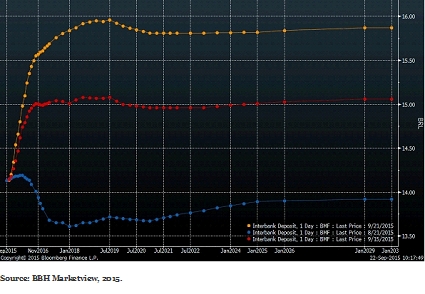

Two of the most ignored words in everyday political economy are credibility and expectations. Everybody talks about the role of fiscal deficits, interest rates, jobs reports, CPI forecasting and other macro policies, but in the end, economic agents are moved by expectations and credibility. And that is what is missing in Brazil today. We can see an interest rate crisis when yields go from 14% in nominal terms to 16% in a matter of weeks, with a concurrent devaluation of 10% in September, 2015 alone.

How did Brazil come to be in such a conundrum? The answer is simple: lack of credibility and sinking expectations. The loss of credibility is due mostly to inaction, expectations followed, and now there is only one path left, the dreaded one. Austerity.

Austerity only works when it changes expectations, anchoring it to the normal dynamics of the broader economy. Half-assed austerity leads to half-assed recoveries. Just ask Europe. Since Brazil has no major political capital to spend on half-assed measures, only a strong commitment to the return of a balanced budget can anchor expectations and derail the spiral of a sinking currency and rising interest rates. There are tentative measures to improve Brazil’s fiscal standing, but they are coming at a huge cost. The government is spending the little amount of political power it has in a rush to distribute high-ranking offices to former allies and create a large enough base that can allow it to repeal the impeachment movement and to vote in new taxes and spending cuts. Yet, it is all being done in a half-assed manner. There is no comprehensive plan, no structural reforms on the horizon, and the signals the government are sending are weak. It is trying to do as little budget cutting as possible, and acting too little too late.

Here is the thing: the next two years will be horrible for the Brazilian economy. The year 2015 is already, and 2016 will surely follow. We either consolidate a plan to anchor expectations and allow a recovery or we can spend the next few years in stagflation purgatory, a basket case country that will come to define what it means to be stuck in the middle income trap. I hate austerity, usually; yet, it also provides an opportunity for market reforms. Selecting the correct market reforms may not pull the economy from recession quickly, but it should generate higher potential growth that may translate into a more robust recovery, should it happen. Dani Rodrik, from Harvard, has a very good point in that not every market reform is created equal. From Rodrik: Well-chosen reforms have very large payoffs, especially when fighting political battles where they really matter and focusing scarce administrative resources on high-return areas. Right now, reforms that bring credibility are crucial, especially in two areas: long-term fiscal solvency, and ease of doing business. Later, labor productivity and improved welfare should come back to the forefront. How we do the first set of reforms is crucial, and I have written before about what they should cover. Here is the painful truth, though, raising taxes should not be a part of any set of reforms, but we cannot escape it. There is a weak commitment to bringing back the CPMF (a 0.2% tax on all financial transactions, a Tobin’s tax on steroids, and I mean Lance Armstrong level of steroids). The commitment should turn into a strong one, and I am now begrudgingly in favor of the CPMF’s return (it was in place from 1994 to 2007). It will have a huge recessionary cost, something that could have been avoided last January, when expectations were of a mild contraction and paltry fiscal results. Now that the deficit has ballooned through inaction, Brazil needs any sign of credibility it can get its hands on. It should not have come to this, but it will be much worse if no major useful reforms follow. Hello there, CPMF, I hope you only came for a brief visit.