When facing a dilemma, you can’t have it both ways. In international finance, the economic theory of the trilemma also requires hard choices. You only get to pick two out of three fundamental options: active monetary policy, fixed exchange rate and free capital flow. Pursue all three, as China recently learned, and you risk bringing yourself and the global economy down.

China is now grappling with an indirect speculative attack on the yuan, a perilous vulnerability the authorities there likely considered impossible given its trillions of dollars in reserve. Regardless of that financial buffer, no matter how massive, they should have known better. You don’t mess with basic economics by ignoring the limits of the trilemma — in China’s case by apparently assuming it could maintain tight control over its money supply and its exchange rate and, at the same time, introduce measures to free up the flow of capital.

China’s current situation is sadly reminiscent of the missteps taken by the United Kingdom and many emerging economies during the 1990s. This time around, the global reverberations have mostly shaken stock markets instead of currency markets because more countries are now keeping their exchange rates flexible. However, that provides little solace given the damage already incurred by Chinese financial policy and the continuing fallout.

As China’s ill-founded attempt to test the trilemma takes its toll globally, the feeble economies of Brazil and Russia appear to be among those hit by the worse collateral damage. Both are suffering massive devaluations, at least in part from the worldwide movement of capital due to uncertainty surrounding the Chinese yuan.

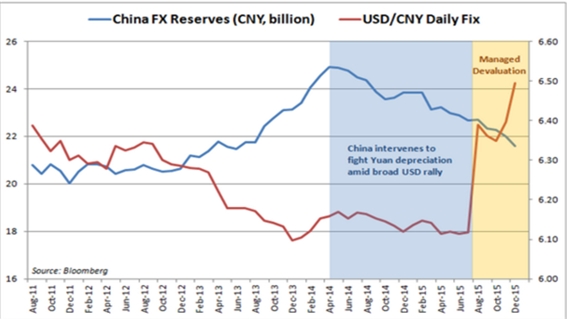

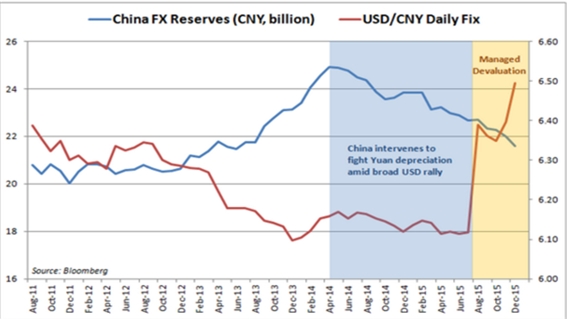

The graph below provides a snapshot of the story so far:

Capital outflows from China started to accelerate in April 2015. In August, China abruptly devalued its currency against the greenback, a move designed to stop the bleeding of capital outflows. Nevertheless, outflows continued to accelerate. About $170 billion left the Chinese economy in December alone — a clear sign of bets against the yuan pegged to the dollar. The move to a peg against a broader number of currencies did not help much, since the exchange rate is still determined daily by the People’s Bank of China (PBOC).

Since then, Chinese authorities attempted a managed devaluation, another breach of basic economics in these circumstances. This gambit, as in Brazil in 1999, hasn’t worked; China can’t fight free capital flows and maintain a managed exchange rate. Massive reserves aren’t enough to keep capital from fleeing the economy.

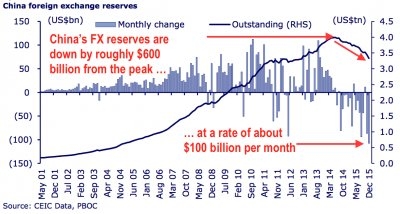

This next graph shows China’s reserves already down $600 billion from their peak, and diminishing at an alarming rate.

What are the possible options to get back on track? Again, the trilemma allows China to take only two of the three paths available. Assuming it keeps a fixed exchange rate it must then either allows the yuan to flow almost if not entirely freely, or it has to tighten capital controls.

Last month, China admitted communication flaws regarding its management of exchange rate policy. Haruhiko Kuroda, Japan’s central bank governor, asked Chinese policymakers to tighten capital controls. Yu Yongding, a former PBOC’s adviser, is recommending that China lets its currency float.

Chinese policymakers no doubt understand the yuan’s predicament. So we can only speculate why China is delaying the inevitable choices ahead. Perhaps there’s fear of shaking the status quo even more than it has been shaken since April 2015, especially only months after the yuan joined the International Monetary Fund’s basket of currency.

Or maybe Chinese policymakers still have faith that the country’s reserve buffer (however diminished), if accompanied by some exchange rate tinkering, could stem the tidal wave of capital outflows, especially if there is an increased market sentiment on a global recovery.

For China’s sake, and the world economy’s, let’s all should hope the right two choices are made soon within the trilemma.