The setting: an executive education class in Manaus, in the Brazilian Amazon. In the room, ultimate owners and their families. Teaching was on optimal debt policy, and we started a discussion on subsidized credit in Brazil.

It was 2012, and we were amidst the height of the Brazilian megalomania; white elephants were being built for the World Cup and the Olympics, hundreds of billions were allocated for oil and energy investments, and the government decreed that the interest rate would fall by 500 basis points. The Selic, the target interest rate in Brazil, went from 12.5% a year to 7.5% a year in 13 months. It did not stop there. The government decided that to stimulate economic activity in the North part of Brazil, which is mostly composed of the Amazon, the Brazilian development bank, BNDES, should offer subsidized credits at a 2.5% annual rate, in nominal terms. Inflation was at 5.5% a year. To recap: BNDES was offering long term credit at 2.5% a year, when inflation was 5.5%; the real interest rate was at -3%, not considering the tax shield benefits for medium-sized and larger companies. Of course, that was not enough: credit was plentiful; it was available to most industrial companies, since the Treasury transferred around USD 100 billion to BNDES to fund the arrogant “neo-development” project of the Brazilian government.

Now, think about the ultimate owner of a medium-sized company. The Brazilian government is offering you a handout. Subsidized credit, with negative real interest rates, to fund whatever crazy idea you have. The rational answer: get as much credit as you can, and enjoy the income transfer from the whole society to a select few (the Brazilian government that professes that they work for the poor rarely does).

I was explaining all of this and the son of the ultimate owner of a large transportation company started furiously arguing with his father. The argument got heated and the whole class stopped. Eventually, things calmed down and he turned to explain what had just happened. They just undertook a project to renovate part of their fleet, 40 trucks in all. He told his father that they should use BNDES funds to do it. He was only able to convince his father to get a loan to replace 2 old trucks. The rest, the ultimate owner argued, they would do with their own funds, from the profits of their operations. We made a simple calculation and the difference in maintenance costs of new and old trucks would more than cover the nominal interests on the subsidized loans, and part of the principal. The -3% real interest rate was most likely -15%, in this instance. What was the argument of the owner of the company for refusing to go to BNDES and ask for funds? He hated incurring debt.

The behavior of ultimate owners in small and medium size enterprises is full of contradictions. The profit-maximizing entrepreneur whose only purpose is to make more and more money simply does not exist; the economics textbooks are wrong. Ultimate owners want to make money, but more often than not, ego is a much more powerful driver to entrepreneurial activity than profits, especially for older and established companies.

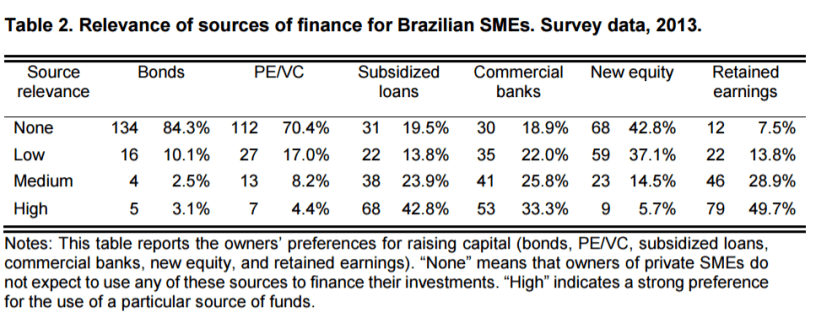

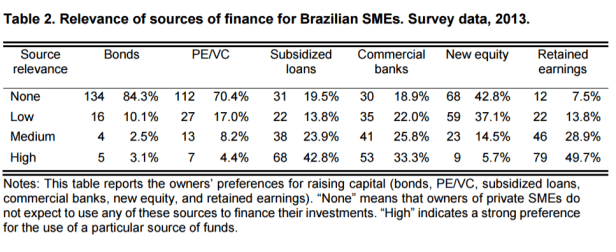

Most ultimate owners are willing to forgo efficiency for growth in revenue. They also have an unhealthy relationship to debt. On a recent research, with Koresh Galil of Ben-Gurion and Offer Shapir of NYU Shanghai, we bring evidence of the strong preference for retained profits, even with the availability of heavily subsidized loans. We look at the Pecking-Order Theory (PET) in a survey of ultimate owners. The PET states that owners have a preference for retained profits, then debt, and only after these two options are exhausted, new equity to fund new investments. We find a lower preference for subsidized credit than for retained profits, which is irrational, from an economic point of view, at least in the setting we were studying. Think about the example in Manaus: the ultimate owner could fund a fleet renovation using subsidized credit at 2.5% a year, or use retained profits (equity) with an opportunity cost of 10% a year (this is a conservative estimate). The owner was foregoing at least 7.5% per year so that he could claim he did not have a lot of debt. Let’s assume that the whole fleet renovation would cost him USD 10 million (it was more). He was throwing away more than USD 750,000 per year because of his ego (or incompetence). The latest version of our paper can be downloaded here.

Most of the finance research in the world is undertaken with American listed companies. But once we get out of the sophisticated American financial system, there is still plenty to study. I usually stress to the ultimate owners of SMEs that at some point they should focus on making money, instead of throwing it away.