The short answer: it depends. This is usually the case in economics and one of the reasons people consider it a dismal science; economists rarely give unconditional advice. So let’s go for the long answer and explain under which conditions fiscal spending can create or destroy economic activity. We will then apply our model to the cases of the US, Japan, Germany, Brazil and Greece.

I just finished writing a textbook on the Economics of Global Business. A huge chunk of it deals with basic macroeconomics for business students. That means that sophisticated models are out. My main goal is to explain how public authorities design economic policies. Nevertheless, there is some technical knowledge required. I will try my best to keep it as simple as possible, but be advised that the infamous supply and demand curves do show up at some point.

Here is the thing that most textbooks miss: economics is context-dependent. There are precious few universal truths. Austerity may destroy social welfare in Germany but enhance it in Greece. The correct prescription also changes over time. Austerity may be the correct path one year and not the next. The same with fiscal spending: context matters. In Brazil, Keynesian economics still rules. By Keynesianism I mean a view of economics that use some of what John Maynard Keynes proposed in his magnus opus “The General Theory of Employment, Interest and Money” but is also informed by some other economists, like Michał Kalecki. My training as an economist came from professors who were unabashed Keynesians. Which is fine, although I missed on learning about the models that were then current, such as Real Business Cycles and Dynamic Stochastic General Equilibrium Models. Here is one of the major tenets of this tropical version of Keynesianism: given the existence of significant fiscal multipliers, governments by spending more create economic growth that justifies the extra spending. Can the Keynesian point of view work? Yes. But it is not universally true, no matter how many professors in Brazil believe it. So let’s define the environment under which expansionary fiscal policy (from lower taxes or extra spending) can create prosperity. By doing so we can also solve one of the main paradoxes of the Brazilian economic history: why the deepest recession in modern history was caused by excessive spending, a counterintuitive turn of events.

Most economists would agree with the following statement: fiscal spending can spur economic growth in the short run. Nevertheless, that does not mean that government expenditures create true prosperity. That will depend on three factors: the amount of crowding out, the impact on aggregate supply, and the public debt trajectory. In extreme cases, like Brazil recently, higher spending can even cause a recession.

To understand why government spending is context-dependent, we just need a good description of the loanable funds market. This is the market for credit, where aggregate investments are determined. This is extremely important, because higher investment drives growth in the short and long run. On the one hand, we have lenders, the agents that supply loanable funds. On the other hand, we have the borrowers, those that demand loanable funds. To simplify things further, let’s assume that people save (supply loanable funds) but don’t borrow, while companies borrow (demand loanable funds), but don’t save. The government can either borrow or save, depending on how it structures its budget. Here is the technical part: the fiscal multiplier depends on the response of the supply curve of loanable funds to government borrowing, and its evolution over time.

We can model the fiscal multiplier as a simple two-stage game. In the first, the government decides to borrow more. In the second, the rest of society reacts. The fiscal multiplier existence depends on the reaction of agents to the decisions of public authorities. Let’s use extreme examples to illustrate what this technical part actually means.

- Governments as drivers of economic growth.

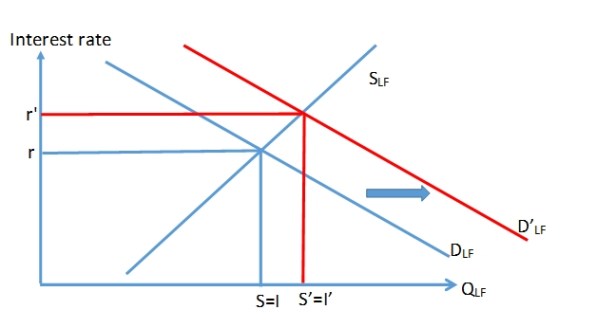

Let’s imagine a supremely credible government that wants to borrow money from society to spend on useful projects, like research and development on green technology, improvements of primary education, or a good unconditional cash transfer program. Just by announcing the increase in spending, companies want to invest more. We summarize sophisticated dynamics into our simple model of step 1: government, step 2: companies and households. If people are willing to supply funds to this government, the fiscal multiplier works, and the third-world Keynesianism taught in Brazilian schools is born.

A simple representation of this on the loanable funds market (Investment is ALL aggregate investment, public and private; ditto for Saving (S)):

The government wants to borrow more (step 1). People are willing to lend more (step 2). Credit is created. Investments increase. Interest rates would not increase, and whatever deficit the government incurs would have no impact on the real interest rate of the economy. Everybody lives happily ever after. Sounds far-fetched? It is. As is the next extreme example.

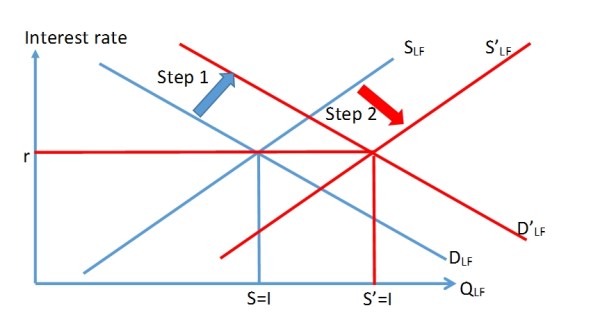

- The liberal dream: the bad, bad governments.

In this example, there is perfect crowding-out. Step one is the same as before. But now agents reduce what is available to governments (step 2), because of distrust. Whenever there is more government spending, the only result for society is higher interest rates. As the government wants to borrow more, it comes at the expense of lower private investment. Public displaces private, and the cost of public (and private) borrowing increases. Budget deficits would be clearly bad for society.

This can happen when governments have little credibility. Think of a profligate authority trying to borrow more and more while delivering bad investments, resulting in an ever-increasing public debt. Lack of trust can cause the public to always react in the opposite direction; people would be trying to protect themselves from an incompetent government. Even if that is true for some countries (hello, Venezuela and Zimbabwe!), there is no way that perfect crowding out is pervasive around the world.

- The context-dependent world.

This is the intuition: governments can be bad when they are incompetent, or good if public authorities are remotely competent (and consistently so). What a crazy idea, right? Verily, it is almost as simple as that.

There are two moderating effects on the link between fiscal spending and economic growth over time: the public debt trajectory and the efficiency of public spending. Let’s use the example of Egypt, where the government decided to to build a new capital and is financing most of the USD 45 billion necessary to erect it with Chinese funds. If the reaction by Egyptian society is to buy into this idea, then all sorts of private investments should happen and the whole society should benefit. If, what is more likely, this turns into a ghost city to rival the ones in China, then the Egyptian external debt will increase without corresponding economic activity.

The fiscal multiplier is context-dependent. The correct model is, of course, usually something in between the two extreme examples.

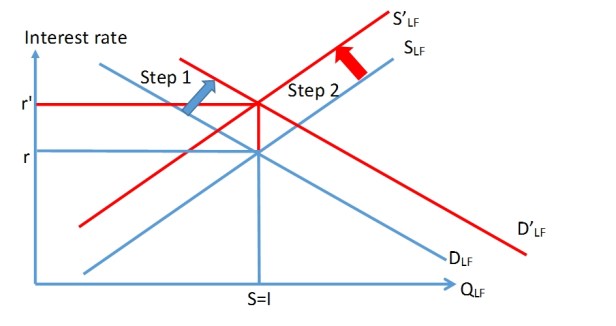

Government expenditure can increase aggregate investment, but at the cost of higher interest rate. Public investment crowds out SOME private investment, but in aggregate economic activity INCREASES.

How does that help us understand the counterintuitive examples of the large Japanese debt, the Brazilian spending-fueled recession, or Greek austerity? Credibility is the main driver of the reaction in our model of public/private investments. And here is something where the original Keynes was right but that it seems to have been forgotten by many contemporary Keynesians: expectations and credibility matter. A lot. Whenever the credibility of governments is high and expectations align with the decision of public authorities, the supply of loanable funds increases and there is crowding in. Government spending is more easily financed, companies invest more, the interest rate does not increase much, and society benefits. Later, the interest rate may even fall, as the economy reaps the rewards from the original decision of public authorities validated by private investments.

But the converse is also true. When there is no confidence in public authorities, any increase in public spending will not result in much aggregate investment. The ratio of debt to GDP increases, and the original decision to increase spending should have at first an effect on the interest rate; if the trajectory of the debt deteriorates, then aggregate investment falls, and spending could result in a decrease in future economic activity. A negative fiscal multiplier.

In this framework, when is austerity warranted? When credibility is really low and government spending crowds out private ones. And that is the Greek conundrum. But more on that later.

Let’s apply what we have learned so far to the counterintuive results in the world economy; we can even use it to make some predictions.

- The Brazilian spending-recession paradox.

Here are the facts: the Brazilian governments went on a binge in the 2009-2016 period. The primary budget went from a surplus of 2% of GDP to a deficit of 6% of GDP. All sorts of crazy projects were funded, from a nuclear submarine to hundreds of billions in tax breaks to many industries. One example: the Treasury transferred around USD 180 billion to the Brazilian Development Bank (BNDES), so it could lend at low and subsidized rates. No aggregate investment came. In the end, it was a simple transfer from the Brazilian government (and all of society) to its elite.

The succession of events: the Brazilian government decides to spend more; it does so by violating a balanced budget law and fiddling with the data; concurrently, its investments are atrocious (Olympics white elephants, anyone?); as this becomes apparent, confidence in the public authorities starts to decline; the government’s incompetence in mustering political support makes credibility shrink further; public spending continues to increase; as the political environment deteriorates, the supply of loanable funds dwindles; the interest rate climbs sharply WHILE aggregate investment decreases. There is complete crowding out. The impeachment comes. A new government has a tight window of opportunity to restore credibility. It is struggling to do so. And that is where Brazil is. There is a credibility crisis. The real interest rate is high and agents are not willing to finance a profligate government. There are only three outcomes to this story:

- The government performs a costly austerity to restore confidence. Given Brazil is amidst its worse recession in modern history (-3.8% GDP growth in 2015 and -3.6% GDP growth in 2016), this is unappetizing.

- The government tries to spend its way out of the recession. Since it lacks credibility, this should result in higher interest rates, explosive debt trajectory and maybe even hyperinflation if total confidence is lost (here is what they don’t teach in school: hyperinflation comes from a total lack of credibility in the fiscal authority that chooses to print money since it cannot issue bonds; hyperinflation is a fiscal, not a monetary issue). Here is the thing: under a normal recession, trying to spend its way out of it is a valid strategy. But not when a) there is no trust in public authorities and b) public debt is increasing sharply. Remember that the fiscal multiplier depends on credibility and expectations.

- Reform the economy to restore confidence. This is the current plan. Brazil needs numerous reforms. The more reforms the government enacts, the more trust in its abilities can be restored. The real interest rate decreases as the supply of loanable funds increases. If enough confidence returns, private investments surge and the country gets out of the recession. But that is a big if. After all, it relies on a horrendous executive power that miraculously attracted some good bureaucrats. Good luck to us all.

The hard truth: if the government had just expanded the Bolsa Familia (a cash transfer program to the poorest of Brazilians) while being careful not to create disincentives for people to work, either the Brazilian recession would have been shorter or there would have been no recession at all. Instead, the stupid Brazilian government spent 50% of GDP on useless investments (and some of it went into the pockets of corrupt politicians). Megalomania destroyed the Brazilian economy. The main problem nowadays: given that the public debt is out of control, fiscal spending is untenable (some Brazilian professors advocate more spending – therein would lie the path to hyperinflation), even amidst a deep recession. Finally, there is a risk of a political free rider who promises instant credibility: vote for me and everything will be alright. Brazil is screwed.

- The Japanese missing explosive debt.

Nothing illustrates better the power of expectations and credibility than the case of the Japanese missing debt “explosion”. Japan has an ageing population while its government has the highest gross debt to GDP ratio in the world. Not only is Japan indebted, but the OECD estimates that Japan’s gross debt should reach over 400% of GDP in 2040. Even so, the country has had an effective interest rate of 0% for most of the 21st century, and in July 2016 the 20-year central government bond yield has turned negative, which means that investors were paying for the right to borrow from a highly leveraged government.

Central to this are two facts: most of Japanese debt is held by local investors; and throughout it all, the Japanese government has retained confidence in its ability to manage the economy.

The credibility of the Japanese government did not change even throughout Abenomics, the program of Prime Minister Shinzo Abe to try to make the Japanese economy recover through public spending. Abenomics was a cry for crowding in. It failed, but it also did not cause a major reaction against the government. Meh.

The main thing about the Japanese conundrum: the government has the credibility to try to spur economic growth through even more public spending, even with a high debt/GDP ratio. Nevertheless, if it fails, it can lose credibility and that would make people sell off the bonds of the Japanese government. This would create more problems than the current economic stagnation. What would you do?

- The Greek conundrum.

The Greek conundrum is similar to the Brazilian one: a lack of credibility on the Greek debt trajectory after the financial crisis of 2007/08 led to successive bailouts by international authorities, an economic depression, and no end in sight to the economic problems of the Greek economy.

This depressing situation also illustrates the importance of confidence as the driver of economic activity: as the debt ballooned, the interest rate that lenders required to hold Greek debt rose, making the public deficit higher, resulting in even more debt.

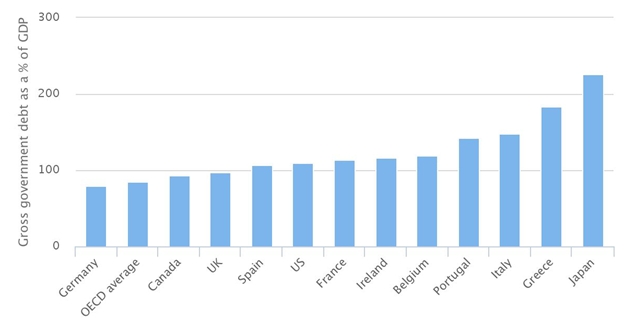

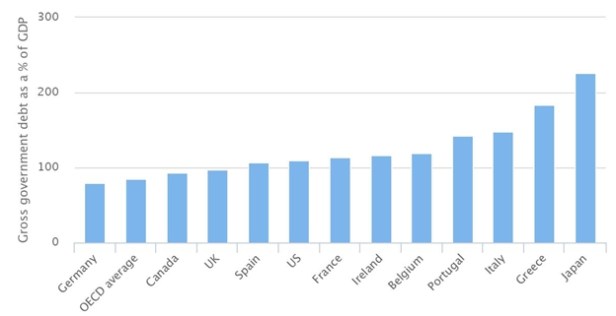

Greece was not alone. From 2010-2015 European countries suffered successive debt crises. Five countries were especially affected because they combined deficits with local financial crises that required a bailing out of the financial system: Portugal, Ireland, Spain, Cyprus, and Greece, with the last one being the worst case.

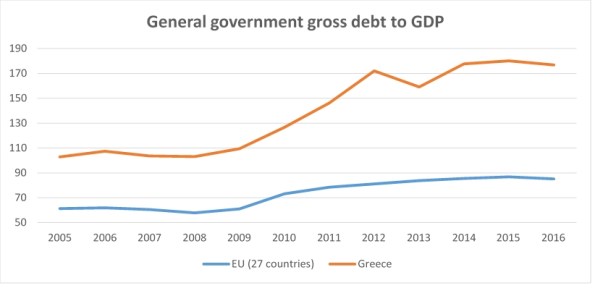

Source: Eurostat.

Source: Eurostat.

In 2008 the Greek debt amounted to a bit over 100% of GDP. It had almost doubled by 2015, reaching 180% of GDP. The deficits in 2009 and 2010 were of 15% and 11% of GDP, respectively. Moreover, in 2011 a renegotiation led to a haircut (discount) of 50% of the value of the government bonds held in the hands of the private sector. The country received three bailouts, in 2010, 2012, and 2015, from the “troika”: International Monetary Fund, Eurogroup, and European Central Bank.

The main issue with Greece is that it should either a) try to restore credibility or b) abandon the euro. It is clear that it is trying the first option, but half-heartedly. Restoring confidence in the fiscal authority is painful. It should be done in a Machiavellian way: “severities should be dealt out all at once, so that their suddenness may give less offense”. Greece is stuck in a dangerous trap: it undertook much austerity, but not enough to restore confidence. This is understandable from a political point of view: austerity is painful. Trying to do as little as possible makes sense for public authorities. But they erred. Credibility is won with decisive action. If it was done before, Greece would be on the path to recovery. Instead, we got a tug of war between Syriza and the Troika. The Greek people lost.

- Donald Trump and his infrastructure plan.

Donald Trump is a buffoon. But America, even given its current political dysfunction, has credibility in spades. If President Trump devises a conceivable infrastructure plan, he can actually achieve the economic growth he is looking for (there are other variables, like potential output restrictions, but I aim to keep this as simple as possible).

After all, this is the market for loanable funds that he faces (unlike Brazil or Greece):

Spending more would generate higher investments, even at the expense of a higher interest rate. If those investments were to be funneled wisely (a big if), the American economy could reap rewards for this idea. Of course, the stupid discourse on restricting trade and immigration is undermining confidence in the President’s abilities to manage the economy. Confidence in the economy makes public spending affect investment, instead of interest rate. Low credibility results in more interest rate and less investment. Less confidence means a lower likelihood that any infrastructure plan will bear fruit. Context dependency is everything.

- The missing hyperinflation in the US, Europe and Japan.

In 2010, a group of economists penned an open letter to the Fed warning of the dangers of inflation following QE. They were clearly wrong. Inflation is still highly irrelevant for most developed economies almost 10 years after the crisis. Round after round of QE, in the US, Europe, and Japan, failed to stoke inflation. In fact, in 2017, Japan and Europe have it as their goal to increase inflation, not curb it. What happened? Hyperinflation can only happen if there is absolutely no trust in the fiscal authority. The group of economists that signed the letter erred because they assumed QE would destroy the confidence in the Fed and the Treasury. It clearly didn’t.

- The perils of German thriftiness.

Finally, we come to the case of German thriftiness and its deleterious effects on the European (and the global) economy. Germany has so much credibility, with a controlled debt trajectory and a relatively balanced budget, that it has the ability to spend more without much drawback.

The Economist was absolutely right when, in 2014, it stated that the German government should invest money in infrastructure, and not worry about balancing its budget. It was right again, when it claimed that Germany was investing too little—hurting Europe, the world and itself. The Economist even tried to bring urgency to the decision of expansionary fiscal policy by German’s public authorities, warning that an historic opportunity to improve infrastructure on the cheap was in danger of being squandered.

In an ever changing world, the German context remains the same as when the Economist started hammering the point that Germany should invest more. Yields on German bonds are negative. There is an oversupply of loanable funds in the country. The government can borrow at negative interest rates. The economy could do better.

If there is a case for a fiscal multiplier, that is Germany today. It is 2017, but the warning of 2014 is still valid: Germany is in danger of squandering a golden opportunity. As long as the government were to spend on “good” investments, like R&D on green technology, education etc, the country and the whole world would benefit.

Governments do not make decision in a vacuum. How companies and people react is quite important. Past actions do come to bite countries in the ass. Greece and Brazil would greatly benefit from spending their way out of their slumps, but successive incompetent governments made sure that they cannot afford to. Japan tried it, but is somewhat constrained by its large debt (past half-hearted attempts) and did not spend enough. The US could try it, but is overseen by a mediocre figure. Germany is truly the only country among these with the ability to spend as much as it wants, but it is stuck in the same mentality that created its credibility in the first place. Would Germany face risks if it went on a spending binge? Hardly, as long as it did not splurge like there is no tomorrow. Then again, maybe there won’t be.

The author is clearly unaware (like almost all economists at the higher levels) that there is a new school of economics around.

http://ingramwebinar01.blogspot.com

This tackles problems which no other school of economics has tackled and is now a course at a university near me.

I left some details at LinkedIn where this essay was also published by a link.

It is posted at the Financial Economics Association at LinkedIn

LikeLike