Interest rates in Brazil are extremely high, easily reaching triple digits – last time I checked, the third largest bank in Brazil offered me the equivalent of USD 20,000 for a modest rate of 121% per year.

The credit market is dysfunctional, with perennial supply scarcity. In a dynamic market, this should attract new players, especially fintech companies, and this market failure should disappear. Unfortunately, nothing indicates that this will happen in Brazil. All details about the Brazilian case are in my latest article for Americas Quarterly.

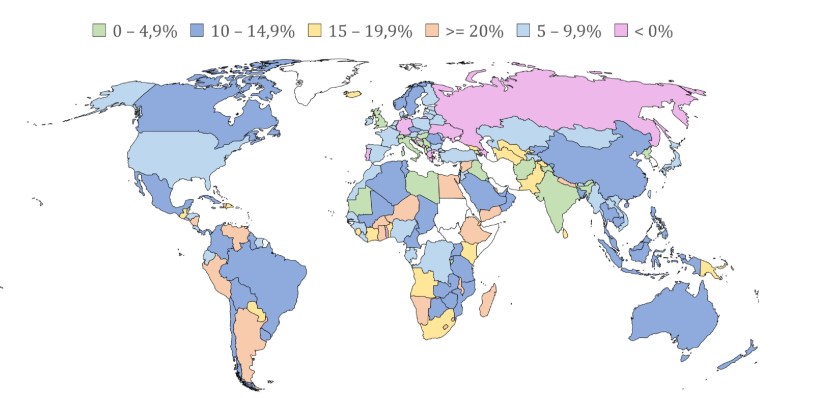

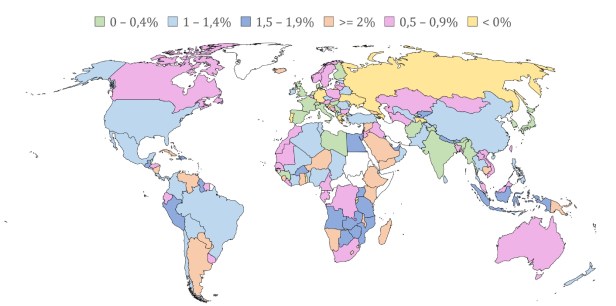

Two figures were left out from the main article: Return on Assets and Return on Equity (after tax) for the banking sector. They illustrate the fact that in Brazil nobody wins. Not the government, the banks or the consumers. The financial system generates expensive credit, and most small and medium-size enterprises are priced out of the loanable funds market.

There are no easy solutions. If there is one thing in which the Brazilian economy differs from the rest of the world is in its insularity. Competition is abhorrent to the Brazilian ethos. The financial authority looks for stability over everything else. This helps breed complacency. The result? Absurd interest rates and banks that lend too little. Nothing indicates that this is going to change anytime soon.