Nothing beats cold hard cash. No company better illustrates this than Amazon – its business model is about cash, liquidity and growth, and not profits. Much has been written about the company, but one dimension is often ignored: the role of trade credit in helping Amazon grow exponentially. Every company needs cash to grow. Some, as Uber, Xiaomi, Switch and AirBnb, will tap private equity; others such as Mars, Bosch and Koch Industries will use past profits, sometimes foregoing exponential growth for a more secure path to prominence.

Negative cash conversion cycle is the overlooked part of Amazon’s plan of global domination. As sales rise, the negative cycle helps the company fund its investments for future revenue growth, in a positive feedback loop that requires Amazon to continue growing. It is a virtuous cycle but not without risk: new markets and products generate more cash (but not necessarily profits), allowing the company to expand its operations. As long as revenue continues to increase, liquidity is not a concern, differently from most companies that pursue a rapid expansion strategy.

Amazon has constantly defied expectations. It is now a behemoth, but for a long time analysts pegged it as a bubble stock; the company does not deliver much by the way of profits, buybacks or dividends. In a world where share buybacks have been compared to corporate cocaine, Amazon has continued to buck the trend. The company grows unrelentingly, but in a world flush with cheap credit, it is surprisingly unleveraged.

The missing link in explaining the successful trajectory of the company is that Amazon has had a negative cash conversion cycle (financial, cash-to-cash or C2C cycle) since its beginning. Trade credit has allowed the company to fund all its investments with money from its supply-chain until the mid-2000s, and even today helps explain why the company does not need to pay dividends, buyback its own stock or generate profits. It also provides a compelling reason for the acquisition of Whole Foods. By integrating the retailer into its existing operations, Amazon should be able to fund almost one third of the acquisition with the cash trapped in the seemingly inefficient financial cycle of Whole Foods. While Amazon’s financial cycle is approximately -94 days, in the last financial statement before being acquired, Whole Foods’ C2C was positive and stood at approximately 4 days.

Trade credit comes from squeezing suppliers and getting advances from customers. This kind of credit is important in many countries, especially emerging nations where companies find it difficult to borrow from banks and where financial markets are illiquid so there are barriers to issuing commercial papers and other forms of debt. It is also particularly important for small and medium size companies and among those, like Amazon, which want to expand quickly.

What is more, trade credit is usually ignored because there is no easy concept to communicate the relationship between changes in payment terms and shareholder value, and because longer cycles might lead to higher costs and shorter cycles to lower sales. The following section seeks to rectify that through the lens of the financial cycle and the operating working capital and its relationship to shareholder value. These concepts are important for understanding Amazon’s impressive growth and the Whole Foods acquisition. The next section will be of most interest to readers who want accounting and financial details on trade credit and firm growth.

Amazon’s business model: financing growth via trade credit.

Financial cycles tend to change as companies mature. Start-ups are usually starved for cash, but do not have enough market power to extract credit lines from its suppliers or require cash advances from its customers. As companies mature, the addition of new products and services, suppliers and consumers results in C2C changes. In Japan, new agreements usually require spot payments, especially from foreign companies. After a few years, as trust is built between suppliers and consumers, payment terms from large to small companies extend to months. Amazon, however, displays a strikingly constant negative C2C cycle throughout its history, even with the addition of distinct services such as B2B cloud storage and content production. Its business model has always been based on exponential growth financed, partly, by its supply-chain.

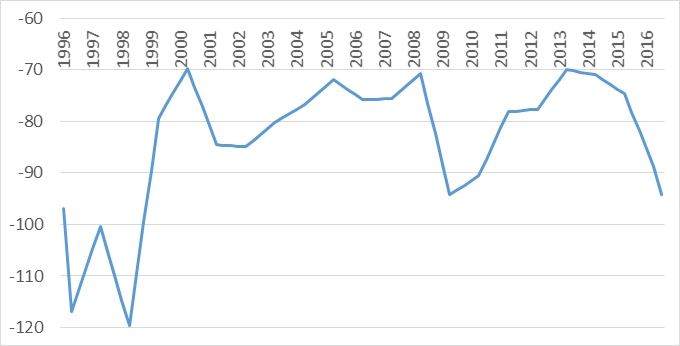

Amazon’s C2C has never been higher than -70 and lower than -120 days – it was -94 days in its latest financial statement. Given this pattern, the growth of the company meant that its operating working capital turned increasingly negative.

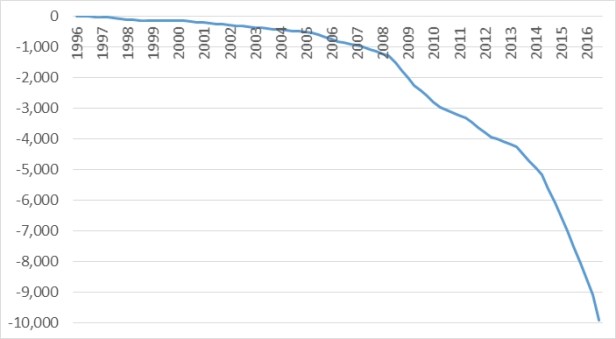

Amazon’s negative operating working capital crossed the US$ 10 billion mark in the third quarter of 2017. Given that the nominal accumulated value of investments throughout the company’s 20 years has been a little over US$ 100 billion, this means that roughly 10% of Amazon’s total investments have been financed by its supply-chain. Even more important, trade credit was the most important source of finance during Amazon’s early days. Up until mid-2003 negative operating working capital was able to finance all the company’s investment. Lately, capital expenditures has been soaring and the company is tapping other sources of capital, but there is little doubt that trade credit is a fundamental part of the company’s growth strategy.

How does this work and where does it end?

The principle behind the cash-generation machine that is key to Amazon’s growth strategy is simple: Customers pay for the merchandise they order immediately when placing an order. Amazon, in contrast, uses its market power as one of the largest retailers to extract payment terms from its suppliers that allow payment at 60 days’ notice and more. For a firm that does not grow, the advantage from such 60 days of free credit is not immense, particularly in times with low interest rates. If the firm is on a growth path, however, say its sales grow by 10 million in 60 days, the 10 million only need to be paid to suppliers with a 60-day delay. If the growth can be sustained, the 10 million can be invested in other projects. This strategy turns really interesting once a firm has exponential (i.e., above linear) growth. In this case, the amount of cash generated from negative cash conversion cycles keeps increasing. If, at the same time, the firm’s market power also increases, and the payment delay extracted from suppliers can be increased yet further, a firm with no profits can generate increasing amounts of cash that can be used for investment.

The crux of such a growth strategy is sustaining, in fact accelerating growth. If growth goes to zero and a firm reaches a steady state in terms of size, the money that was loaned from suppliers needs to be put into operations as working capital. In this situation, only reducing cash conversion cycles remains to generate cash flows without profits. A company will try to use its market power to pressure suppliers into granting ever longer payment notice. Once it has maximized that, it can acquire other businesses with long cash conversion cycles and reduce those, as Amazon will do with Whole Foods’.

Amazon Prime, the Whole Foods acquisition and the value of constant inflows.

Aswath Damodaran, one of the top valuation professionals in the world, estimated that Amazon Prime, with its 85 million members, contributes around US$ 61.3 billion to the overall US$ 542 billion market capitalization of the company (as of November, 2017). Prime not only enhances the company’s value by locking in customers that spend almost twice as much non-Prime users, but it is also a cash-flow generator. In the US, Prime customers pay US$ 99 per year for the privilege of future discounted shipping and access to video and music services. Prime is more than a branding, value-enhancing proposition for customers; it adds much needed cash which allows Amazon enough liquidity to ignore calls for buybacks and dividends.

The 96% renewal rate makes Prime a boon for a company that has been built on growth that relies on constant cash inflows to help fund it.

The Whole Foods acquisition made headlines worldwide and illustrates another aspect of trade credit: market power and the ability to tap value that is unavailable to the original company.

Many large retailers have negative cash conversion cycles. Since margins are razor thin for companies such as Walmart and Carrefour, negative financial cycles allow them to generate cash and finance growth limiting the need for other sources of capital. For both companies, C2C has been around -10 days, while Walmart’s operating margin is significantly higher than Carrefour’s (4.8% and 1.5%, respectively).

Amazon’s model is clearly distinct from other giant retailers, but there is one common aspect: all rely on trade credit to finance growth and compensate low operating margins. And it seems that Amazon saw an opportunity in scooping up one of the few retailers with a positive financial cycle. By doing so Amazon can use economies of scale to extract trade credit from Whole Foods’ supply-chain without affecting its operating margin, freeing up cash tied in Whole Foods operations. The total operating working capital of Whole Foods was US$ 212 million at the time of its acquisition. If Amazon is able to lower Whole Foods’ CCC to -94 days, it could potentially unlock US$ 4.2 billion, more than one third of the amount it paid for the company. Even in more realistic scenarios, in which the CCC just turns negative without affecting Whole Foods’ operating margin due to Amazon’s better supply-chain management, there will be capital unlocked that would make the retailer a cash generator as it grows.

Amazon continues to expand its empire using its supply-chain capital. Further growth likely will make it even easier to access trade credit. Bezos once said: “Your margin is my opportunity.” We should add: their suppliers’ cash flow is Amazon’s opportunity. At the end of the day, nothing really beats cold, hard cash.