Can one make money day-trading based on sustainability strategies? I don’t think we have gone so far, but we already know that sustainability issues have significant impacts on the value of non-financial companies. If one is a value investor, there is no doubt that ESG factors (Environmental, Social and Governance) directly affect an investor’s portfolio. Just ask BP shareholders who held the stock before the Deep Horizon event how they feel about their shares sliding more than 50% over their peak value. Yet, we still don’t have a comprehensive framework on how to capture the eco-premium that can be generated by sustainability strategies. Here I want to link sustainability issues to the valuation (and thus strategic movements) of public and private firms.

The world is still stuck on a trade-off between financial and nonfinancial performance. Going beyond this trade-off means that we first need to integrate sustainability into regular corporate finance and valuation models. The reason simple – we need changes from inside the financial world and we either make the trade-off easier or get rid of it altogether by proving how sustainability issues generate value to shareholders. We simply cannot regulate our way out of the climate conundrum we face. We need help from small and large companies, investors, and everybody in-between. Some would argue that these issues are already incorporated into the value of public-listed companies, as markets should use all available information for the determination of stock-market prices. However, there is a clear distinction between value and price, and stock prices, in particular, are affected by momentum, liquidity constraints, and other factors. Information on sustainability issues to deliver valuation models is scant even for public-listed companies. Acquiring such information is costly, and that is why it is sometimes hard to estimate the impact of sustainability issues on the value of businesses.

There are some proactive actions by banks to bridge the gap between financial and nonfinancial performance – two of my recent papers are based on this idea, but here I want to showcase the broad ways in which banks and firms can create value by incorporating sustainability issues in their decision-making processes.

A simple framework to relate sustainability and firm value.

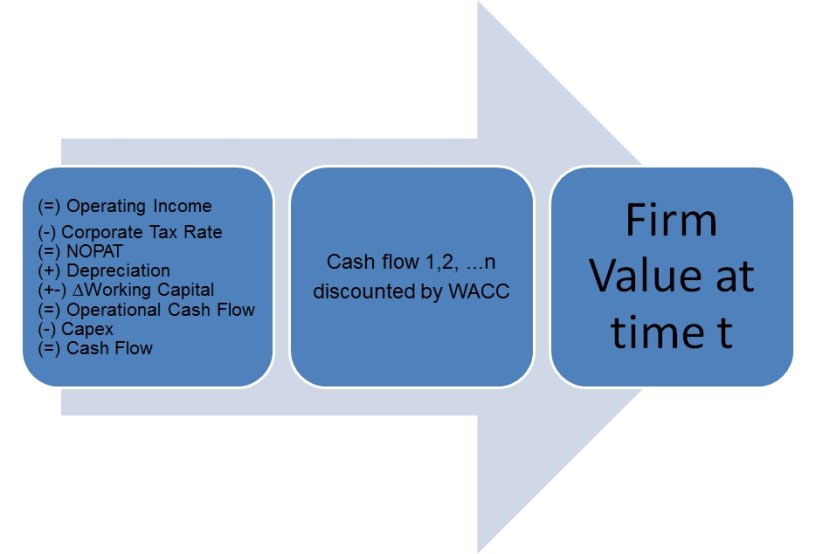

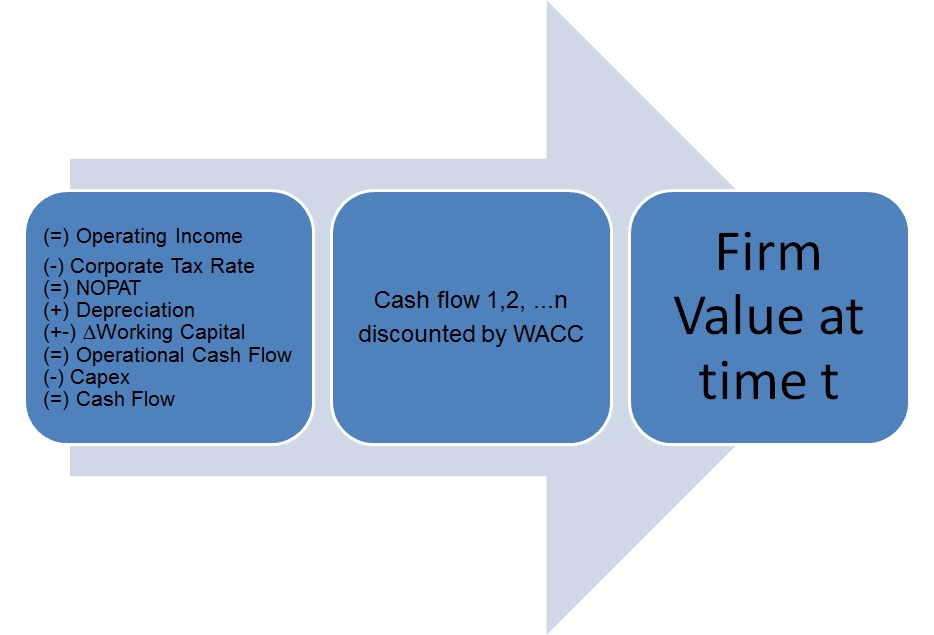

Using a discount cash flow (DCF) method to value a company is a mix of art and science (if you want to learn more about valuation models, I cannot recommend Damodaran’s site enough – he is simply the best valuation professor in the world). The science part is the cornerstone of every corporate finance book: the value of an asset is the present value of future cash flows that are discounted by some sort of interest rate – for companies, the weighted average cost of capital (WACC).

Sustainability issues affect firm value through direct and indirect effects on cash flows and the discount rate of said flows, even without taking into account new concepts such as shared value and eco-premium. We can measure these effects and there are some promising initiatives regarding the evolution of sustainable banking and finance. The main impacts of sustainability on firm value are:

Risk Management

Risk management has been the raison d’etre of incorporating sustainability in the financial planning of companies. It is behind the Principles for Responsible Investment, which are based on the mitigation of ESG risks and have, as of this date, 1369 signatories divided between asset owners, investment managers, and professional service partners. Still, it comprises only a fraction of the millions of companies and asset managers around the world.

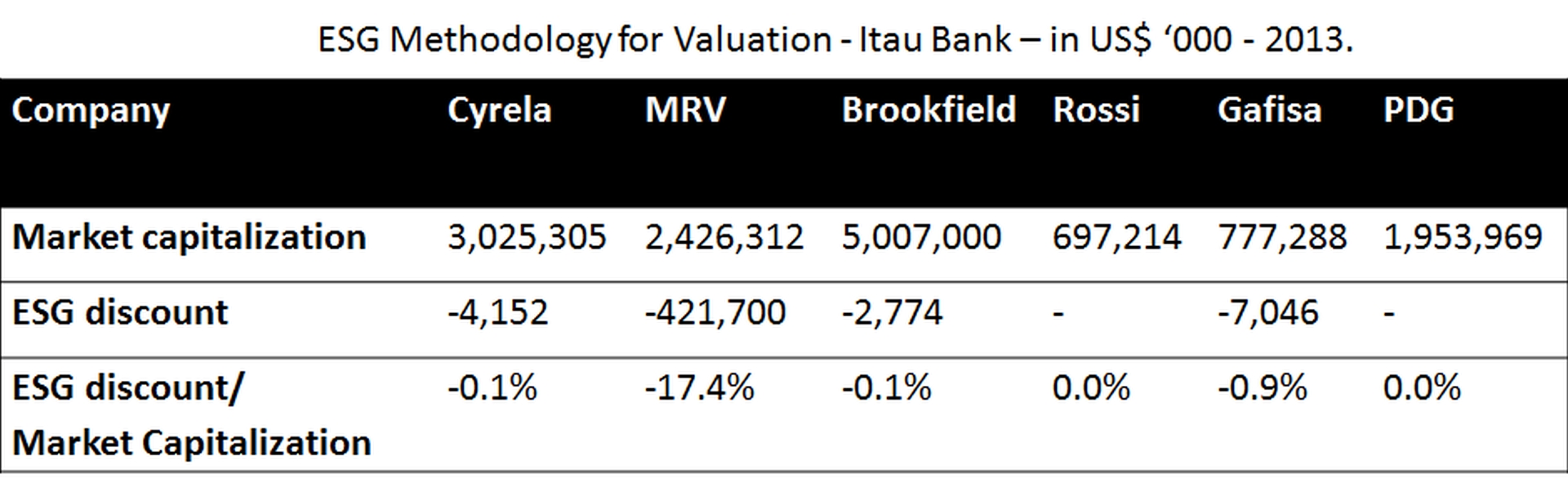

In a paper with Heiko Spitzeck we present the case of Itau, the largest private Brazilian bank that started using ESG factors to alter its portfolio allocation. Below is a table in which Itau analysts create an ESG discount for public companies in the real estate sector. It shows a steep discount for MRV, that made analysts change its weight in the portfolio of their particular fund.

ESG is already an established way to talk about sustainability risks to firms and investors. It is the cornerstone of sustainability reporting for most listed companies. Yet, the main obstacle towards the spreading of ESG factors as a risk management tool for firm valuation or portfolio allocation is related to the measurement of the impact of ESG factors on companies cash flows (what is called materiality). Later I come back to this point, when discussing possible paths to improve risk management models that incorporate sustainability criteria.

Operating costs

Sustainability is costly. There is no doubt about that. Pollution was the price of progress, but now it needs to be avoided by costly processes that treat chemical residues, solid waste, and lower the carbon footprint of nonfinancial companies. Regulation usually increases the cost of doing business, which is translated into higher operating (and investment) costs. There is one question we cannot readily answer, though, and it is: how much do costs rise over time due to sustainability issues? Budgeting sustainability properly should yield this crucial information for predicting future cash flows, but companies usually do not present information on capital budgeting and operating costs and expenses related to environmental or social issues. At most, we get information related to CSR policies, but companies should disclose information on costs associated with prevention of environmental damages, for instance. Improved vehicle standards and regulations regarding fuel efficiency will surely increase production costs, but figuring out the amount allows us to measure the impact on future cash flows.

Revenues

Companies can capture an eco-premium by producing goods and services in a more sustainable ways. This has been done successfully for years by companies like Natura, and more recently, Unilever is trying to capture value by focusing on more sustainable lines of goods and services. Consumers are increasingly willing to pay more for more sustainable products and services. Markets should keep expanding and the more consumers are educated, the higher the growth rate of eco-friendly goods.

CAPEX

Companies need to invest in more sustainable means of production. How much does sustainability cost to each individual company? Same as in the case of operating costs, companies should disclose better information on investments that are related to increased production and those for compliance or transformation of means of production.

WACC

This is probably the best way for companies to capture value due to sustainability actions. We already have clear evidence that improved environmental risk management is associated with a lower cost of capital. Banks are developing sustainability credit score systems to increase or lower interest rates of less or more sustainable companies. Lowering the weighted average cost of capital has a tremendous impact on firm value. A simple example: in November 2014, Damodaran estimated that Vale had an estimated value of equity of US$99.93 billion (his spreadsheet can be found here), given an 8.91% cost of capital. Now, let’s assume a drop of 1% in the cost of capital of Vale, to 7.91% (granted, a significant drop). Vale’s equity increases to U$120.38 billion, a premium of over 20%. Both the sudden drop in cost of capital and increased valuation may seem implausible, given that financial markets are efficient at using existing information to derive good estimation of value and prices of listed companies, but a significant decrease in cost of capital is plausible for many privately-owned companies that need access to external finance.

The mechanisms by which the cost of capital falls with improved ESG management are clear and direct (from NBS):

- Greater willingness of debt markets to provide debt financing

- Higher tax benefits that partially offset the cost of debt capital

- Reduced cost of equity capital from a decrease in systematic risk

I can add easier compliance to loans’ covenants and access to subsidized funds from local and international agencies. Given the potential benefits from the lower cost of capital, firms should have increasingly higher incentives to pursue improved ESG management.

On Cash flows and Strategy.

I agree with Eccles and Serafeim. Sustainability in financial services is not about being green, it is about making money. As markets evolve, banks establish improved risk management tools that go beyond ESG factors, and companies start capturing eco-premiums, a positive feedback loop can be generated that funnels resources to more sustainable companies. It is not a path without obstacles, of course. Fiduciary duty is one of them – we need better cases to prove that ESG management create value, and funneling resources to more responsible companies should increase return on a portfolio while complying with the fiduciary duties of asset managers.

Sustainability management changes future cash flows of firms, and companies can capture increased value by investing in sustainable means of production that increase revenues and lower risks, but, more importantly, decrease the cost of capital. In the next post, there will be the case of a sugar industry in Brazil, which increased its value by investing in bio-energy and organic sugar.