John Cochrane (the great grumpy economist) has a new post on the covered interest rate parity.

The Merton-Scholes-Grumpy fallacy emerges from the design of an arbitrage opportunity when none exists. Let me try to make an argument on why this is a fallacy. First, let me be clear, John Cochrane is one of my idols[i]. But here it goes.

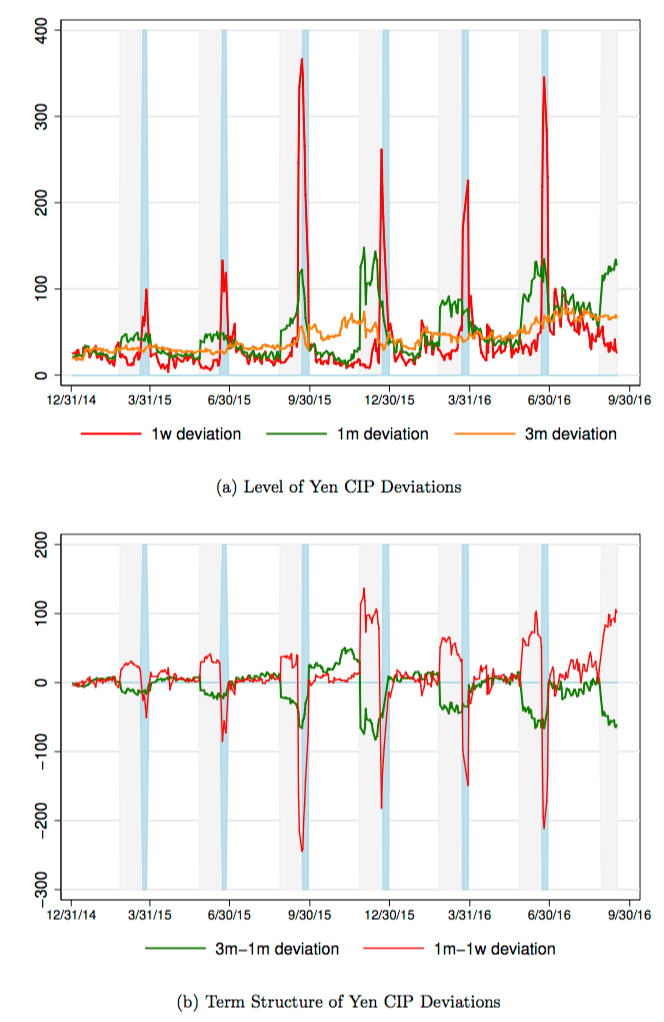

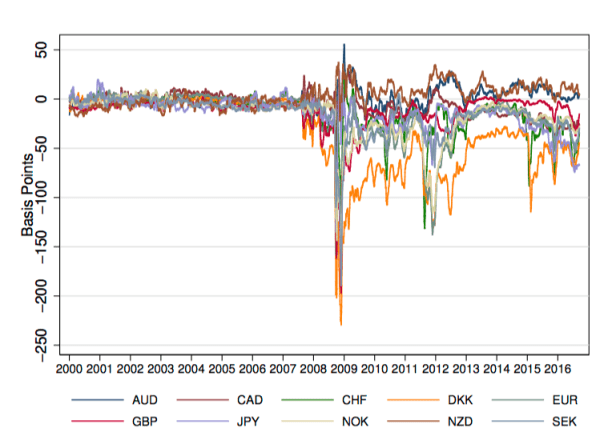

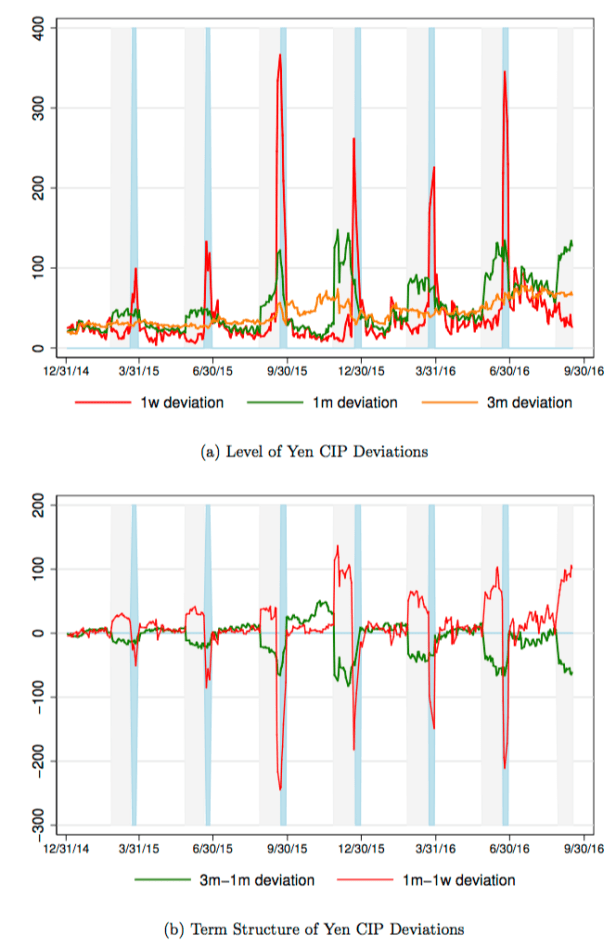

The setting: the yields on government bonds of ‘risk-less’ countries are diverging. Economic theory (and common sense) dictates that exchange-rate adjusted government bonds should pay approximately the same rate of return. Cochrane describes the issue much better than I could ever possibly do. He uses the recent work by Wenxin Du, Alexander Tepper, and Adrien Verdelhan, “Deviations from Covered Interest Rate Parity“, for recent evidence that the differences in interest rate among developed countries is not disappearing, as it should. The graphs below come from Du et al, via Cochrane’s blog.

Not only there is persistent divergence but there is a pattern in which the divergence is much higher at quarter-ends.

The puzzle is how this can keep on happening. Cochrane describes the situation as an arbitrage opportunity: “this makes no sense at all. Banks are leaving pure arbitrage opportunities on the table, for years at a time. OK, maybe the Modigliani-Miller theorem isn’t exactly true, there is some agency cost, and the cost of additional equity is a little higher than it should be. But this is arbitrage! It’s an infinite Sharpe ratio! You would need an infinite cost of equity not to want to eventually issue some stock, retain some earnings rather than pay out as dividends, to boost capital and do some more covered interest arbitrage.” Here is the catch: there is no arbitrage!

I believe that, as in the case of LTCM, liquidity risk explains this. We keep forgetting the lessons of the LTCM collapse: Long-Term Capital Management: It’s a short-term memory. Robert Merton and Myron Scholes were among those that designed the strategies of Long Term Capital Management (LTCM), a hedge fund that blew up spectacularly in 1998, almost detonating a global financial crisis. The strategy of LTCM? Converging interest rates. European and American bonds should yield similar returns. LTCM saw any small divergence as an arbitrage opportunity. Because divergences were tiny, the only way to make money was to make big bets. LTCM leveraged its equity manyfold. But when the Russian crisis happened, because the European financial system was tied to Russia and the US system wasn’t, yields on European bonds surged. LTCM was betting exactly on the opposite happening; that European bonds yields would converge to Treasuries. LTCM lost USD4.6 billion in 1998. The Fed had to arrange a bailout of a hedge fund to prevent a financial crisis.

Here we are, almost 20 years later. Cochrane is incensed over an arbitrage opportunity. But I believe that there is no such thing here. LTCM played the convergence game and lost. The reason? Liquidity and basis risk. Marking to market may create an infinite demand on cash from whoever tries this trade. The convergence game brings these risks: Eurozone collapse; Trumpocalypse; Chinese hiccups; and Italian bank crisis; these are just some of the macro issues. We can add regulatory uncertainty and flash crash possibilities, and all the other reasons in Cochrane’s article (transaction costs etc). Even if a trader establishes a short-term converging strategy, there is nothing to guarantee that strong divergence won’t happen during the trade’s time-frame. Because covered interest parity has not been working, there is all the more reason to believe that there is no arbitrage opportunity. What is more, calling arbitrage with past data is a bit iffy. Claiming that because these quarter-end effects have happened the next one will be like it feels like a 1970s revival of adaptive expectations. Mind you, somebody might still try to play the convergence game and make a bucketload of money in the process. But arbitrage it ain’t.

A simpler explanation. Assume you are the head of a hedge fund and decides to try your hand on the convergence game. You see a spike in yields differential. Are you sure that no strong divergence in the period of your contract will deplete your cash flow? Would you bet USD 120 billion, like LTCM, on that? Maybe with somebody else’s money?

[i] Cochrane’s writing tips for PhD students shaped the way I write. Go read it. It is fantastic. His top-notch research leaves me in awe. This is no faint praise; economists are not like that. But even the great ones err, and the beauty in science is that you can always call it like it is.